You May Also Like

Cash is King, but Value Creation is a Family’s Long-term Goal – Even During a Crisis

Cash is King, but Value Creation is a Family’s Long-term Goal – Even During a Crisis

Compounding Your Family’s Wealth: Building a Multigenerational Family Enterprise Wealth Portfolio 2021

Compounding Your Family’s Wealth: Building a Multigenerational Family Enterprise Wealth Portfolio 2021

Wealth Strategy

Wealth Strategy

Every first generation entrepreneur succeeds by taking huge risks and pursuing opportunities regardless of the available resources under his control. The one common trait is passion— passion about the business and the belief that their judgment about the market is right even in the face of naysayers who discourage them. Because of this passion, entrepreneurs tend to be very attached emotionally to the business that created their initial wealth. The original business is like another child, which is sometimes difficult for founders to assess objectively.

In the beginning, a business family’s wealth is determined by the success or failure of the original business. When the business is growing, the entrepreneur puts all of his limited capital into the business and hopes that the business makes it to wide adoption by its target customers so that the business gets to the minimum scale for it to be profitable. If he succeeds in doing that, at some point, the business starts creating extra cash flow beyond what is needed to support the current scale of operations.

At this point, the family’s wealth accumulation may not necessarily have to be tied to the original business. The business family has three general options:

- Further invest the extra capital generated by the business back into the business to continue growing;

- Deploy some of the capital in other operating businesses with good growth potential and in which the business family has expertise; or

- Create a diversified financial portfolio for wealth preservation

What is important here is to shift the mentality of the family from focusing on the success of the business as the measure of the family’s success to focusing on the growth and risks embedded in the family’s overall asset portfolio. The mentality should become how does the family grow its overall wealth over time and meet the family’s needs from generation to generation, rather than how does the family grow the company over time. This means that the family needs to rise above the company view to develop strategies for the family’s wealth with the original company as part but not the entire strategy.

The main reason that this shift is needed is because once the family has accumulated some level of wealth, the original business may or may not be the primary driver of continued wealth accumulation for the family. Whether it is or not depends on many factors such as where is the industry along its life cycle, what is its competitive position within the industry, and are the next generation interested and capable of leading this type of business.

However, in order to make this shift in mentality, the founder needs to get some distance between him and his founding business, become less emotionally attached to it, and therefore gain more objectivity.

DRIVERS OF FAMILY WEALTH GROWTH AND DECLINE FROM GENERATION TO GENERATION

Every culture has their own saying describing “shirtsleeves to shirtsleeves in three generations.” Why is there a natural tendency for families to lose their wealth over generations?

Here are a few key reasons:

- Families do not have the optimal strategy for allocating their capital for growing the overall family wealth, including an objective plan for the core business based on industrial life cycle and competitive landscape;

- Families lose their ability to make sound business decisions to grow their wealth in later generations. Part of this may be the result of owners becoming more distant from the management of their wealth;

- Lifestyle expectations of family members increase. This results in increase of consumption, which decrease the level of capital that can be used to generate more wealth over time;

- Family members grow exponentially, faster than the growth of wealth over generations. Therefore, the per capita wealth tends to decline. (Note: this may not be as big an issue in certain countries such as China where government restrictions on child births limit the rate of family growth from generation to generation)

In order to keep families financially alive, the business family needs to grow family assets at a greater rate than the family or its business or other activities are consuming them. Consumption of family assets happens in different ways:

- Core business activities/investments that lose money

- New investments where some bets pay off, while others don’t

- Ownership splits among family owners and divorces that reduce investable assets

- Family activities and expenses that don’t produce financial returns

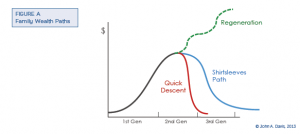

Therefore, in order to sustain and keep growing their wealth, business families need to make one or a few large bets with prudent risks in order to grow their wealth in every generation. Figure A shows the three general paths that family wealth travels over time from generation to generation. The ideal path is for families to regenerate their wealth in every generation, where they create a new source of generating significant wealth. The second is the shirtsleeve path where family members do not take huge risks with their assets, but wealth dissipates over time with consumption and growth of the size of the family group without new sources to replenish it. The last is the quick descent path where families make big bets in risky ventures and lose their family fortune.

For a business family to be on the wealth regeneration path is not easy. In order to achieve this, the family needs at least one wealth generator in every generation. Furthermore, there are hard choices that need to be made about how family members would work together, how to manage the family wealth, how much to be managed collectively and individually, what sacrifices family members are willing to make in their lifestyle in order to put capital to work in generating more wealth. We have observed from over three-plus decades of working with business families that families need to focus on three areas simultaneously in order to be successful: (1) Develop sound asset growth strategies; (2) Maintain unity within the family; and (3) Focus on developing talent, both family and non-family.

OBSERVATIONS OF ASSET GROWTH STRATEGIES OF SUCCESSFUL BUSINESS FAMILIES

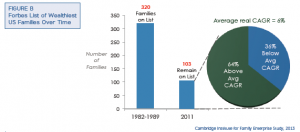

At the Cambridge Institute for Family Enterprise, we have been conducting research on the growth and decline of family wealth from generation to generation for the last year and a half. In one part of the research, we used the Forbes 400 list of the wealthiest US business families from 1982 when the list was started to 2011 in order to capture the families who have stayed on the list through this entire period. We analyzed similarities among this group of business families who have been successful at achieving high growth of their family wealth from generation to generation.

Initially, the Forbes List had 320 families on the list from 1982 to 1989. Out of that 320 families, about 30% of the families survived on the list until 2011, as seen in Figure B. The majority of the families who have survived on the list achieved an average growth rate of their wealth above the 6% average long run growth rate of large US public equities. If the family has a diversified liquid portfolio of financial assets, it could achieve this average. In order to achieve a long-term growth rate above this, the business family needs to find more attractive investment opportunities that tend to be higher risk.

On further examination, we find that most of the 103 business families who have remained on the Forbes from the 1980’s until now have not switched to passive financial investment, as shown in Figure C. Instead, they are still involved in operating businesses. Being involved in operating businesses does not necessarily mean that they remain in the legacy business in which the family’s initial wealth was created. It also does not mean that family members are directly involved in managing the business. But it does mean that the family has significant influence over the operating businesses either as members of the company board or as shareholders with a guiding voice.

This brings up the issue of how do business families think about the strategy of managing their overall wealth and how their decisions regarding their core businesses fit into this bigger picture. Business families’ initial wealth usually comes from a successful operating business. Once that original business overcomes the first growth challenges to achieve attractive profit margins and predictable cash flow, the family arrives at the point where it can shift its focus from growing the business to planning for the business within the context of growing the family’s overall wealth.

Here, the central question that families face is what are their options regarding the business and how should they decide? From this point onwards, the family is not fighting for survival of the business as the only path to wealth creation. This is the time to step back and look at the company’s prospects more objectively. Looking at it from the lens of the industry life cycle is very helpful. In Figure D, we show a generic industry lifecycle.

Usually, a successful founding entrepreneur finds a new industry or niche market. He rides the wave of the explosive growth of the market and becomes a dominant player by beating out many other competitors. That is why in the creation stage of the industry life cycle, the industry tends to have many players. As it enters the growth stage, the industry tends to consolidate into a few players who achieve wide adoption by customers and have the financial strength to invest in the growth while sustaining losses. During the growth stage, winners become large and profitable. Then as the industry reaches maturity stage, the company continues to be profitable or perhaps even improve in profitability, but revenue growth slows or begins to decline. Towards the end of the growth stage is when business families establish their wealth base and should start looking at their options.

Looking at Figure D, which summarizes the key talent needs in each stage of the industry life cycle, the founding entrepreneur is usually skilled at the creation stage and maybe the growth stage. But once the company reaches the end of the growth stage, the expertise and view point needed is that of an investor. Based on our experience working with first generation founders, they are ideas and operations people. They do not have the investor mindset. And this is where they often falter.

Assuming that the founder has the foresight to understand that a shift in mentality and skill sets are needed, there are still many options available to business families. And families have pursued these different options with great success. The key to success is to incorporate three factors into the decision about the business.

- Understand the realities of their industry and competitive landscape so that feasible options are generated;

- Identify and effectively deploy the core competencies and talents of the business plus larger family enterprise; and

- Take into account the desires of the family members

Possibly options for business families at the end of the Growth stage might include:

- Diversify into other geographies within the same or adjacent industries; or

- Diversify into different industries within the same geography

An example of successful international diversification within the same industry is the large Brazilian steel company Gerdau, which is controlled by the Johannpeter family in Brazil, now in the 4th generation. The four brothers, Jorge, Frederico, Germano and Klaus were at the helm of the business for most of the last 35 years, during which time the brothers decided to expand and diversify their operations outside of Brazil

The Johannpeter brothers decided to expand their operations outside of Brazil in part to reduce their financial exposure to Brazil, which until the mid-1990s was a comparatively closed economy with high inflation and low growth. They decided to do so within their core steel business, as they believed they had developed strong competencies in managing steel businesses in difficult environments.

However, in order to make the strategy work, the brothers knew that they had to build consensus around their decision and make sure that everyone is mostly support of each diversifying acquisition. This approach worked very effectively. By 2002, Gerdau was the largest producer of long rolled steel in the U.S. and well over 65% of Gerdau’s business was outside of Brazil. Gerdau is currently amongst the top 12 or 13 steel producers in the world with a strong presence in the Americas and Europe.

An example of a successful industry diversification within the same geography is the Ayala Corporation in the Philippines. It is owned and run by the Ayala family who are of Spanish-German descent and started the business family in the 19th century. They have long roots in Philippines, know the country very well, and have a highly reputable family brand there. They used this core competency to help them diversify across a variety of industries within the Philippines. Currently, the family has business interests in real estate, finance, telecom, and utilities.

Direct investments under the direction of skilled business people and investors tend to yield higher returns. But because these investments tend to be less liquid and bear higher risks, the family really needs to know what it is doing and what fits its needs in order to make the right decisions. This means that at least one family member needs to be a wealth generator in every generation. The wealth generator role is primarily one of being the steward of the family wealth. The wealth generator does not necessarily have to involved in the day to day operations of the business. But it has to develop and implement the asset growth strategy of the family.

For example, the well-known Italian industrial family—the Agnelli Family—who owns Fiat Motor Company is now headed by the young 37-year-old business leader John Elkann. John Elkann is the Chairman of Fiat, the largest source of the Agnelli Family’s wealth. He is also the Chairman and CEO of EXOR, the investment company that holds the Agnelli Family’s ownership in Fiat, the real estate firm Cushman & Wakefield, some financial institutions, and the Italian soccer club Juventus. Mr. Elkann is not involved in the day to day management of any of these operating companies in which the Agnelli Family has significant ownership stake. However, he oversees the family’s overall wealth strategy and form the family ownership group’s views on the future of each of these operating companies.

Based on our research, effective wealth generator may differ in personality or work experience, but the one common trait that they possess is being a change agent. Every generation faces different economic or business challenges and has a different set of family members with their distinct interests plus dynamics. Therefore, change is critical in every generation in order for the family to “keep up with the times” and be reinvigorated.

Beyond that, it is important for family members to remain united in their goals and support the wealth generator. The family leader who helps the family group maintain its unity needs diplomacy and good political skills. It may be that the wealth generator is not equipped to accomplish that. This is why often times, there are 3 key groups within the family that need to be developed in order to create longevity within the family enterprise.

The roles need to be cultivated include:

- A few wealth generators who can develop and implement strategies for regenerating wealth in every generation;

- Some family leaders will maintain unity within the family in support of the wealth generators; and

- Generally, capable owners who understand what the leaders are trying to accomplish and are willing to buy-in to the approach and make sacrifices when necessary

Having this base of capable, educated owners is extremely important. It builds the foundation of stability for family enterprises to be able to keep its assets together and grow them effectively. In the example of John Elkann of the Agnelli Family, he became the family business leader at the young age of 28 when his great-uncle Umberto Agnelli passed away. The family’s key business holding Fiat Motor Company was in trouble at the time. Umberto was the chairman of Fiat at the time of his death. The non-family CEO of Fiat—Mr. Marchio—used this opportunity when both the Agnelli family leadership is weak and the company is weak, to pressure the family to make him both the Chairman and CEO of Fiat. Up to that point, the family has always had a family member at the helm of Fiat to guide it. Mr. Marchio is trying to strong arm the family into breaking with this tradition. He threatened that if the family did not give him the duo CEO-Chairman roles, he would quit. If the family agreed to it, the result would have been that the family’s influence in Fiat would decrease over time.

John Elkann, the untested young family leader decided to he would like to replace Mr. Marcio with Mr. Marchionne who had been a long time employee of the family enterprise in another part of the business empire. But in order to make this bold move without hurting family unity, he called a family meeting, which gathered together the 100+ family owners, to ask for their input. The enlightened family recognized that despite Mr. Elkann’s age and inexperience as the family business leader, they have confidence in him and in the belief that a family member needs to lead the family’s business interests. With the family’s backing, Mr. Elkann let Mr. Marchio go and installed Mr. Marchionne as the CEO of Fiat. This turned out to be a very successful move. Mr. Marchionne since then helped turn around Fiat and expand the company into the US by buying Chrysler.

This example shows that a business savvy wealth generator is needed. But equally as important, the family enterprise need enlightened family owners who are educated in the nature of family enterprises to be able to back the wealth generator during key turning points when risky decisions need to be made.

John A. Davis is a globally recognized pioneer and authority on family enterprise, family wealth, and the family office. He is a researcher, educator, author, architect of the field’s most impactful conceptual frameworks, and advisor to leading families around the world. He leads the family enterprise programs at MIT Sloan. To follow his writing and speaking, visit johndavis.com and twitter @ProfJohnDavis.